Can You Write Off Car Insurance on Your Taxes

Your insurance premium and your deductible are the two types of payment you'll make related to insuring your car, and there are certain circumstances under which each can be written off or deducted from your taxes.

Your car insurance premium is tax-exempt only if you use your car for business, and you can subtract your insurance deductible from your taxes, but the process can be complicated.

For instance, you can't simply subtract your insurance deductible from your taxable income. Read on to learn more about when car insurance is deductible, and how to file your tax forms accordingly.

- When is your auto insurance premium tax-deductible?

- Writing off your car insurance deductible

- Keep accurate records for tax filing

- How to deduct your car insurance on your tax forms

When is your auto insurance premium tax-deductible?

If you own a car you use exclusively for business purposes, then all costs associated with the vehicle— including gas, maintenance and insurance premiums—are deductible as business expenses. For example, if you are a self-employed contractor and need to drive your supplies around in a truck, which can be expensive to insure, then you may deduct your premiums from your taxes.

There are some crucial nuances to understand before writing off your car insurance.

- A car you use to commute to and from work doesn't qualify as a business expense, and therefore does not qualify as tax-exempt. As such, you can't write off any car-related expenses related to commuting.

- You can't write off your car insurance if your business or employer already reimburses you for the cost.

You can partially write off car insurance if your car is used for both business and personal Use

If you drive a car for both personal and business reasons, you may deduct your insurance costs from your taxes for the percentage of the time you use your car for business. If half the time you use your car for business, then you may deduct 50% of the yearly auto insurance costs on your taxes.

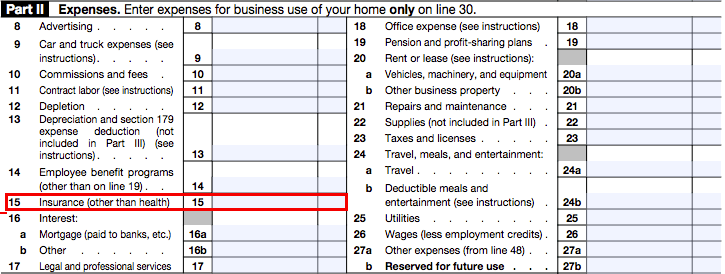

People who don't usually use a car for business but occasionally drive somewhere for their employer can also take advantage of this tax break. For example, if your boss asks you to attend a meeting that requires you to drive to the location, the cost of insurance for the time of the business trip is deductible. It's not deductible, however, if your employer reimburses you for the insurance.

Airbnb Owners and Renters

If you operate an Airbnb or rent a home, any travel expenses related to maintaining the home are tax-deductible. So if you drive to the house for the purpose of upkeep, cleaning or to let in a guest, you are allowed to write off the insurance for that trip.

Keep in mind that if you only do this once in a while, or do not drive far, the deduction will not amount to much since it will ultimately be a small part of your total driving throughout the year. But if you frequently make trips to your rental property, the savings can add up quickly.

Uber and Lyft drivers

If you drive for a rideshare company, you may need to have special insurance to protect yourself and your passengers. For the time you use your car as taxi, your auto insurance is deductible.

If you are required by state law to have rideshare insurance that goes into effect while you are driving, you can deduct the entire premium for that coverage from your taxes.

In addition, if your state and insurance company allow you to use your own personal insurance while ridesharing, you can calculate your deductible time by dividing your monthly car insurance payment by the percent of time you use the car for ridesharing.

For example, if you drive two hours every day getting groceries, picking up kids, etc., and then drive three hours for Lyft at night, you can say you use your car 60% of the time for ridesharing (three Lyft hours/five total hours per day). So if your monthly car insurance premium is $120, you can deduct $72 per month or $864 per year.

Writing off your car insurance deductible

Starting in the 2018 tax year, you are generally unable to deduct personal losses due to casualty or theft, regardless of whether or not the loss is covered by an insurance policy. There is one exception: property losses that occur within one of a few federally-mandated disaster areas and are a direct result of the disaster. For example, in 2017, the only disasters which would have qualified under this rule are Hurricane Harvey, Hurricane Irma, Hurricane Maria and the California wildfires.

If you experience a financial loss involving your car as the result of such a disaster, you can write it off on your taxes. However, you can't write off any loss for which you were compensated for, such as by insurance. In other words, you can only do this for the dollar amount you actually lost. This typically means that you can write off your car insurance deductible or the repair cost if your car is damaged in a way that is not covered by your insurance.

Additionally, you must subtract $500 from the amount of loss in order to determine how much you are able to write off.

For example, suppose you had a car worth $15,000, and it was destroyed in a wildfire. That type of damage would be covered under comprehensive coverage, which is optional.

- If you had comprehensive coverage with a deductible of $1,000, your insurance provider would pay you $14,000. Then subtract $500, and the remaining $500 would be deductible.

- However, if you chose not to have comprehensive coverage on your car, you wouldn't receive any compensation from your insurer. But you'd be able to write off the entire value of the car, minus $500, as a loss: in this case, it'd be $14,500.

Keep accurate records for tax filing

If you qualify to deduct car insurance expenses from your yearly tax bill, then you need to keep good records. One of the key perks of rideshare driving is flexibility: You may drive five hours one day, one hour the next and seven another day.

If you drive sporadically for your business, knowing how much you drove during the year can be difficult unless you are keeping steady track throughout the year. Write down every time you were driving on the clock, and also have a good estimate of all the times you were off the clock.

You should hold onto those driving records for at least three years. Should the IRS ever ask you to justify your car insurance tax write-offs, you will need to be able to show them.

How to deduct your car insurance on your tax forms

If you are self-employed, including as a rideshare driver, you will file a Schedule C tax form, which includes a section to include your deductible insurance expenses. If your business driving was for an employer from whom you receive a W-2, you will file a Form 2106, Employee Business Expenses for those deductions — assuming your company did not already reimburse you for the costs.

Below, see where to fill in car insurance expenses on your Schedule C.

Keep in mind that you can only write off insurance expenses if the total amount you're eligible to deduct exceeds the standard deduction.

However, car insurance expenses rarely amount to more than a couple thousand dollars a year. As a result, you would likely need to have more deductions, such as business expenses, mortgage interest or certain education expenses, to be eligible for itemized deductions.

Consult your accountant if you're unsure

It's best to do your taxes correctly the first time: A few dollars saved is not worth the time and expense of a possible audit. If you're unsure about whether you're eligible to deduct your car insurance from your income taxes, consult an accountant or someone well-versed in tax law.

If you're doing your taxes using services like TurboTax, the company will have on-call customer service with trained accountants ready to answer your questions. If you use your own personal accountant, be sure to consult with them.

Can You Write Off Car Insurance on Your Taxes

Source: https://www.valuepenguin.com/is-car-insurance-tax-deductible